Revealed

SMART SAVERS

How artificial intelligence and a few mobile apps can add up to huge savings

From Cleo to Plum, we give the lowdown on the apps that claw back the cash through investing and analysing your spending habits

From Cleo to Plum, we give the lowdown on the apps that claw back the cash through investing and analysing your spending habits

THE start of the financial year this month means it is a good time to make a resolution to save more for the future.

To help you get in the habit, there’s a whole load of support at hand on your smartphone.

An array of apps and online services have been developed, which work out how much you can afford to set aside, and skims money from your bank account to keep it safe.

Some may be wary of these kinds of services because, at the moment, you still need to share your bank login details with the providers for them to access your information.

That could be a problem if there is fraud on your account.

Banks may refuse to refund losses if you give your login details to a firm that is not authorised and regulated by the Financial Conduct Authority or another European regulator.

But soon it will feel much safer to use these services.

The launch of “Open Banking” means banks and building societies will have to provide authorised firms with information about what is in your account, if you consent to it.

That will mean you won’t have to give away your bank passwords.

But in the meantime, this is still necessary as the technology is being developed and won’t come in until later this year at the earliest.

At the same time, some of the services that already exist, such as Cleo and Plum, are in the process of getting full FCA authorisation.

Today Mr Money looks at how they can help you to save for the future.

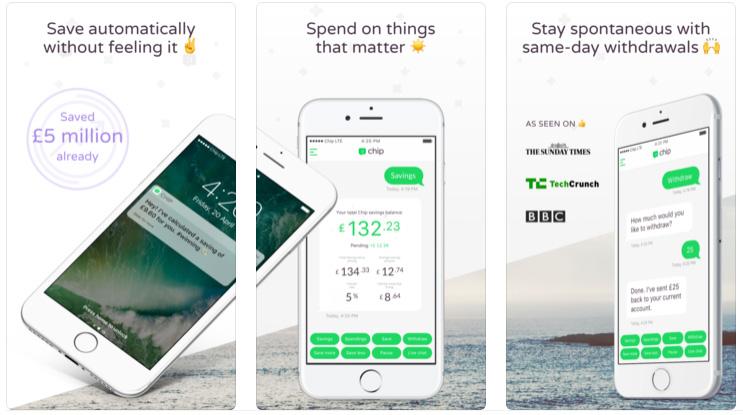

AN automatic savings app. It has access to your bank account and uses artificial intelligence to analyse your spending habits.

It works out how much you can afford to put away and every few days it moves across a small amount, between £5 and £25, into your Chip savings account at Barclays.

When you download Chip you start on zero per cent interest. But you are given a unique code to refer friends and each one gains you one per cent interest.

You can refer up to five friends and this interest lasts for one year.

The cash doesn’t have the usual £85,000 per person protection via the Financial Services Compensation Scheme (FSCS), but bear in mind the real risk is if Barclays rather than Chip goes bust.

Chip is FCA-regulated as an agent of the e-money firm Prepaid Financial Services (PFS), which provides Chip’s savings accounts.

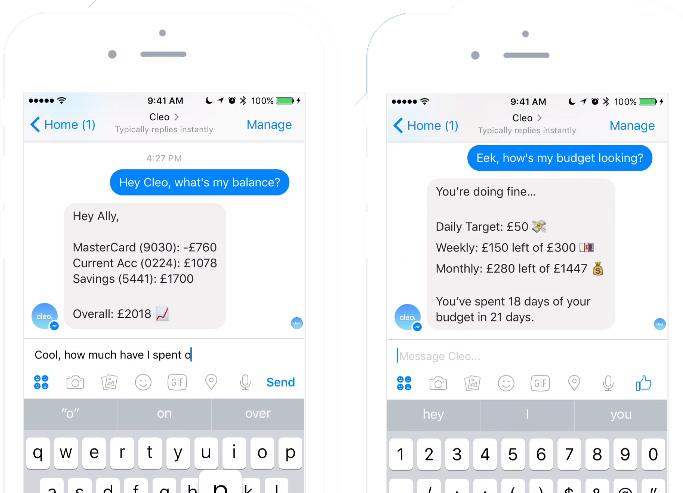

THIS is a “chatbot” – a robot you can talk to – that “lives” in Facebook Messenger.

It works in a similar way to Chip. You link it to your bank account and it works out how much you can afford to save.

It transfers small amounts into your Plum savings account using a direct debit to your bank account.

The savings are held by the electronic money firm Mangopay, which uses Barclays to store funds in segregated accounts.

There is no interest, but users looking for a return can choose various investment options with different risk levels.

Plum is not covered by the FSCS, but the firms says that if it or Mangopay shut down, your funds will be returned to you.

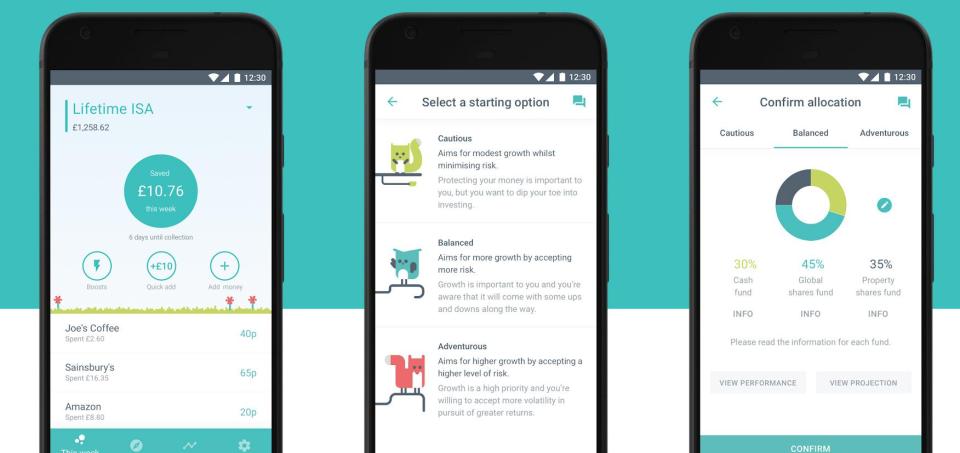

MONEYBOX allows clients to invest small amounts in the stock market by rounding up card payments to the nearest pound.

The app moves users’ digital spare change into one of three passive funds according to their desired level of investment risk – cautious, balanced or adventurous.

Customers can get started with as little as £1. You can also save through weekly or one-off deposits and payday boosts.

If a user chooses to contribute money using round-ups, they need to enter their banking log-in details, which gives the app read-only access to your account. Moneybox can also just be used as a savings account.

The service charges a subscription fee of £1 a month and a platform fee of 0.45 per cent per year, charged monthly. There are also fund management charges, which range from 0.22 to 0.24 per cent per year.

Investments are covered by the Government’s Financial Services Compensation Scheme up to a limit of £50,000 in the event that Moneybox is declared bankrupt. It is FCA-authorised.

ANOTHER artificially intelligent chatbot that operates through Facebook Messenger.

You grant it read-only access to your online banking so it can monitor your money habits and give a breakdown of your outgoings. You can ask it questions to help you budget.

As with Plum, it also calculates how much you can afford to put away per week, then moves it for you into your “Cleo wallet”, which is provided through Mangopay.

The amount taken out is based on your spending and balance, and its developers say you’ll never go overdrawn as a result of saving.

The app is not covered by the FSCS, but it has a voluntary pledge to cover its customers on deposits of up to £85,000. Cleo is not yet FCA-regulated but is working towards it.

TEACHER Vicky Raynes, 34, from Sileby, Leics, has saved £780 through Plum after signing up last June. She says:

Before Plum, I was saving nothing. It’s a way of making sure I have a little pot of extra cash when I need it. It’s like a sneaky squirrel taking one nut at a time to make a huge stockpile.

I trust Plum not to take too much and leave me short. I love the ease of the Messenger Bot, it’s much easier than logging into banking apps and faffing about with passwords.

If I do need some money back in my current account, it’s just a couple of taps away.

I have a car loan and credit card debt all consolidated into a personal loan. I am using Plum to save money and overpay on the loan to pay it back faster.

I’ve still got at least 18 months to go but when that’s gone I will use Plum to create savings and invest.

HEIDI LIGHTFOOT, 29 and pictured, an anaesthetist from Winchester, Hants, is saving into her ISA and a Lifetime ISA through the Moneybox app. She says:

I read up on Moneybox and thought the round-ups idea was a really good one. I liked the fact you could save a little bit of money at a time, so wouldn’t notice it.

Before Moneybox, the only investment product I had was a Help to Buy ISA but I hadn’t been actively investing in it.

I am now investing regularly through Moneybox and don’t even think about it any more. I’ve added the round-ups into my monthly outgoings, and it’s money I don’t miss.

The fact I can also do the whole process through my phone is an added bonus.

With my previous ISA I had to go into my bank to pay the money in. This is a much more convenient option.

6,000.000+downloads/Free/Bengali/Version2.3.4

777 BDT IPL 2025 Sports First Deposit Bonus